Michael Vorwerk

CNS Report

At JFK Club

The

JFK Air Cargo Association Luncheon on November 17, 2011 was held at

the International JFK Airport Hotel and featured as guest speaker Mr.

Michael Vorwerk, President for Cargo Network Services Corporation (CNS).

He is IATA Regional Director Cargo Americas, covering Canada, Central

/Latin America and Executive Director for Cargo 2000. Mr. Vorwerk covered

in his talk CNS updates, an industry overview, discussion of the Global

Cargo Agenda and E-Freight. The

JFK Air Cargo Association Luncheon on November 17, 2011 was held at

the International JFK Airport Hotel and featured as guest speaker Mr.

Michael Vorwerk, President for Cargo Network Services Corporation (CNS).

He is IATA Regional Director Cargo Americas, covering Canada, Central

/Latin America and Executive Director for Cargo 2000. Mr. Vorwerk covered

in his talk CNS updates, an industry overview, discussion of the Global

Cargo Agenda and E-Freight.

In introducing CNS, Mr. Vorwerk reminded

the audience that the corporation had been founded in 1985 “with

the objective of providing support to the newly deregulated air cargo

industry”. While factually correct, it didn’t explicitly

mention that this was after IATA lost its anti-trust immunity in the

U.S. Another interesting tidbit was the statement that “CNS is

structured as a “for profit” company and all our surpluses

are re-invested in industry development and reducing participation costs.

Its parent company, IATA remains non-profit in name and structure, but

equally has been acting de facto as a “for profit” organization

– a very fine line that is!

Next the CASS e-billing system was mentioned with its 2011 billings

of $5 billion and the “adjunct to these services”, the provision

of industry statistics based on data from its billing system, community

information and distribution services that leverage its nationwide network

of airlines and endorsed agents with 1,200 Agents and 2,500 offices

in the USA.

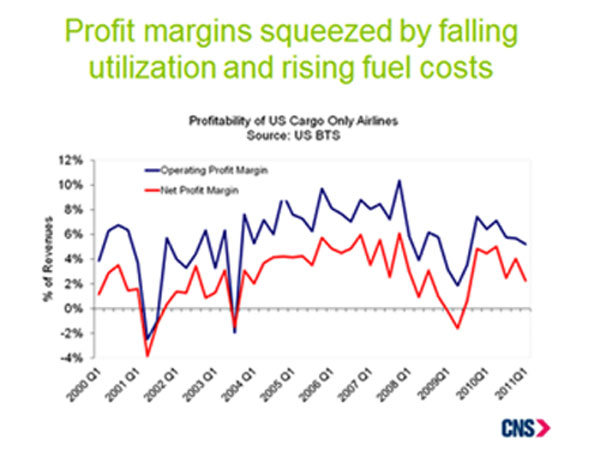

Talking about the falling margins, as

shown below, over the last 10 year period, Mr. Vorwerk remarked that

it was not unusual in the cyclical aviation business and this was the

reason airlines always found the decision to make capital investments

a difficult one.

Having largely recovered from the 2008-09

recession by 2010, and profitability back to acceptable levels, airlines

faced the rise of oil prices in Q4 which impacted the cost of jet fuel

and again profits declined. “Since then margins have been on their

way down, oil has continued to show price volatility but with a definite

rising trend and therefore margins going forward will become even smaller,”

said Mr. Vorwerk. Oil and jet fuel prices remain remarkably high given

the economic gloom and remain 30%-40% higher than 2010 levels. If we

have a recession then they will fall sharply, and if we muddle through,

then high fuel costs will remain a challenge

At the same time, in response to IATA surveys regarding whether volumes

and yields were rising or falling over the next twelve months, the results

for the period from March 2006 to April 2011 indicate that the consensus

was that volumes will continue to grow – marking a certain level

of confidence compared to earlier surveys - but only a slim majority

now expected yields to improve over the next twelve months, which is

a further deterioration in the position at the last survey.

The latest survey in October showed,

most expect volumes to hold up over the year ahead but the outlook for

yields is weakening. “The business inventory cycle is a key driver

of major turning points in air freight; whenever inventory/sales ratios

get out of line. While this looks OK for the time being, a fall in expected

sales, due to the general economic gloom, could have raised the inventory/expected

sales ratio in recent months and contributed to the latest fall in air

freight,” according to Mr. Vorwerk.

He went on to say that “once inventories

had risen to normal levels relative to sales, shippers no longer needed

more expensive airfreight to quickly get products to sales facilities

or components to production facilities. However, restocking is not the

only reason for using airfreight – so we could expect to see further

expansion of air cargo as final sales of consumer and capital goods

continue to grow back”.

The “good news” until April

this year was that world trade has been growing since 2009 and looked

poised to continue; however, world trade has stopped growing, which

is worrisome. In late 2010 the weakness in air freight was because of

losses in market share (partly commodity and trade lane effects as well

as mode [sea, road] shift), whereas now overall world trade is weakening

as the economic situation deteriorates.

The question arises that with inventories restocked,

yet world trade not growing, what are the implications for business

and its propensity to spend? This is where consumer confidence plays

a big role, as illustrated below:

“It’s a mixed bag”

says Vorwerk, “in Europe, represented by the red line, they have

lost confidence, with weak economies in the region coupled with tighter

fiscal policy and high unemployment that have caused the growth in confidence

to stall.

“Here in the U.S. they also lost

confidence, cutting spending on products manufactured and shipped from

Asia”. The figures in green are for China, a positive, where Chinese

consumers and consumers in other developing economies remain confident.

This will provide some support, but these consumers are still relatively

small compared to the U.S. and Europe.

So having taken a look at what airline

heads of cargo think, what business in general thinks, and what consumers

think, “we zeroed in on a group that should carry more weight

than most – purchasing managers,” says Vorwerk.

As global business goes, purchasing managers

in manufacturing around the world are a good indicator of trends. They

seem to have lost confidence, pointing to continued weakness. Their

actions usually lead growth in air freight by 2 months and they are

saying that they will not be increasing orders, which in the past has

at least meant an impact on the growth in the air cargo market.

To complete the sweep, we also have views

from economists; generally most forecasts still point to some growth

hotspots in Asia and Latin America while the view is that Europe may

‘muddle through’, in which case 2012 will see another year

of 2-speed economic growth, yet a European recession would likely drag

down the U.S. and Asia.

In the good news category, to sustain

some optimism, Mr. Vorwerk believes that despite such volatility in

the air cargo market, it is perhaps worth reassuring ourselves that,

in his opinion at least, despite these challenges, there will be an

ongoing demand for airfreight, and despite the current inhibitors, the

underlying drivers will still produce mid-single digit growth for the

global airfreight market in the short and medium term.

A case in point here at JFK, looking

at figures from the CASS statistics, we see that the global trend is

reflected locally. First quarter figures show a volume increase of +5%

year on year, with a corresponding increase of 12% in value.

The top 20 destinations from JFK indicate

clearly a volume impact with far east destination like Shanghai, Hong

Kong and Seoul; for Europe we see strong growth into BRU.

Moving on to the global cargo agenda,

Mr. Vorwerk said “if we take steps now to address some of the

underlying problems in our industry we can turn this downturn into the

basis for a stronger & better future”. This comprises “protecting

the industry’s cash through CASS, adopting and expanding e-business

measures, continued quality efforts with Cargo2000, work on safety and

security and last, but not least, the environment.

He indicated that all the necessary information

concerning the e-freight documents was available on the IATA web site,

together with the IATA handbook and local field resources. Keeping the

benefits in mind was important as these include lower costs, better

service, regulatory compliance and increased security. Equally, if not

even more important are key factors such as data quality and timeliness

which require the evaluation of internal processes and supply chain

performance, with Cargo2000 the industry’s quality system of performance

metrics and reporting. Vorwerk extended an invitation to an ongoing

dialogue with shippers and all other stakeholders improve communications.

Touching on IATA secure freight, he reiterated

the need for a harmonized global approach, securing cargo at the point

of origin rather than security checks for transfer cargo and the pilots

in Mexico & Chile in 2012. In the U.S., efforts are underway to

obtain recognition by the TSA for secure freight.

An ambitious tour de force from soup to

nuts, with few surprises, except no word about GACAG and what makes

CNS unique in a sea of CASS operations.

Ted Braun |